When more traditional investors talk about crypto, they often refer to the asset class as a single large block. A unified investment asset that includes blue chip crypto like Bitcoin and Ether, medium cap projects like Solana, and meme coins like Dogecoin.

And while all these projects have characteristics in common: they are all on the blockchain and have a decentralized approach, they are all different.

In this case, I'm not just talking about the fact that they have different proposals, teams, and adoptions but also different market performances.

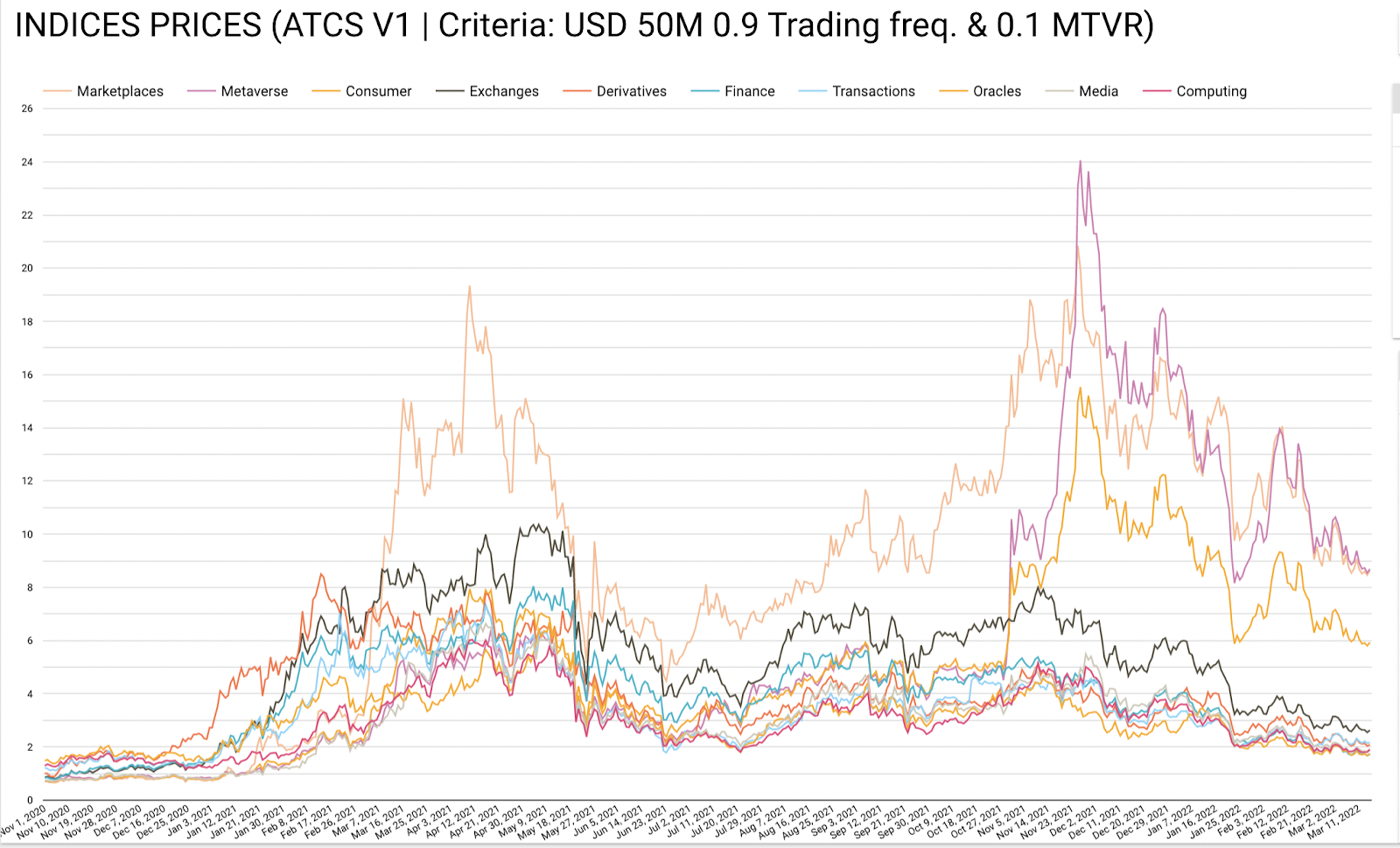

We are on the "anniversary" of the cryptocurrency ATH; just one year ago, many projects - and the financial market as a whole - were reaching historical highs. To see how they have evolved, we analyzed the different sectors and industries of the market, and we came to some interesting conclusions.

For this, we use the data in Arch Intelligence, the platform where we track more than 1,000 tokens in 4 different networks with a market capitalization of more than $650 billion.

The projects that had higher ATHs were the ones that felt the impact of the drop the most.

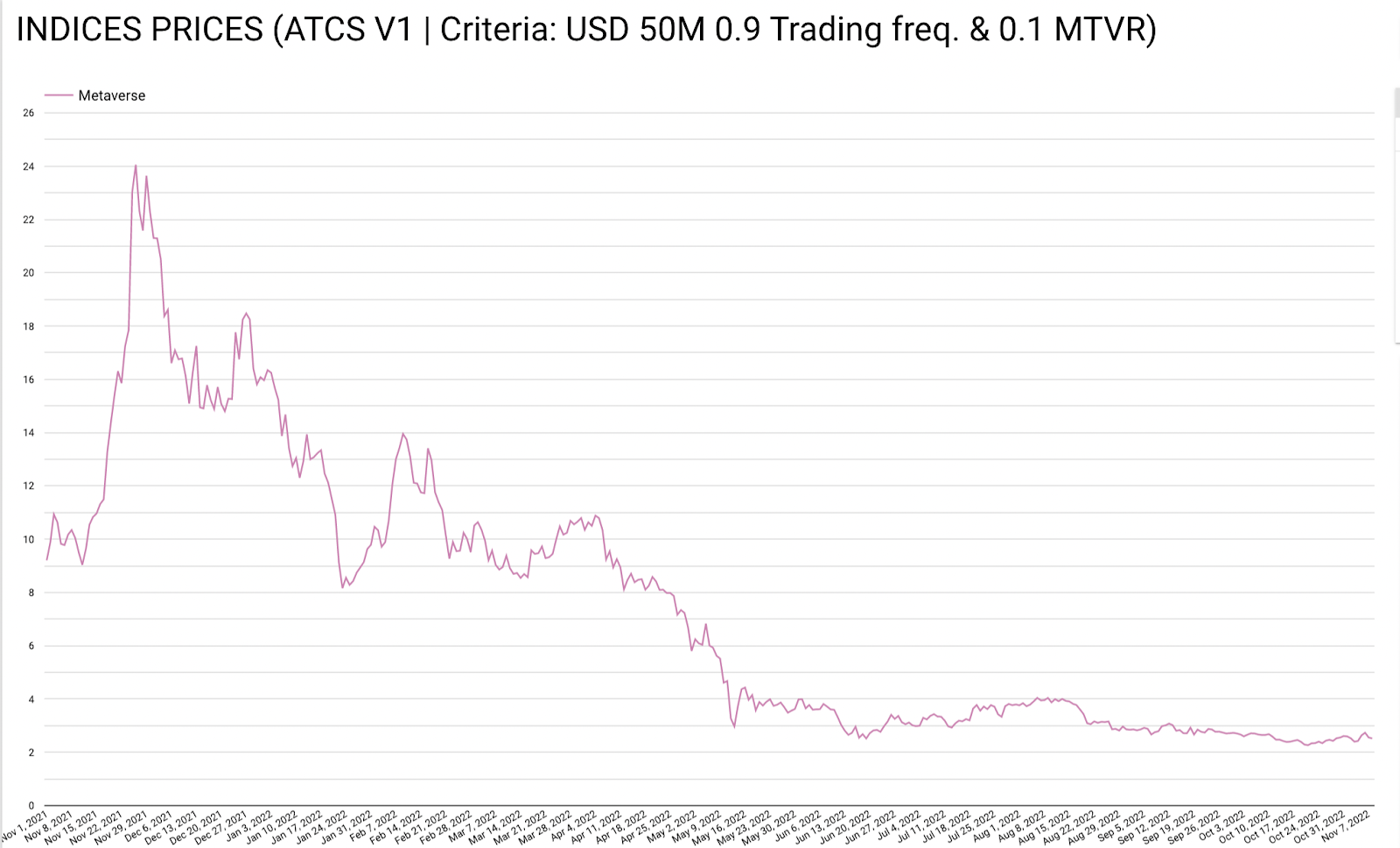

The metaverse sector - which includes projects that have generated excellent media impacts, such as Decentraland and The Sandbox - was the one that felt the impact of the bear market the most, losing more than 21 points from its ATH and reducing by 89.5%

Why? Several reasons predominantly caused by the fall in prices and purchase volumes that NFTs have experienced.

However, it is also the industry sector with the most significant institutional adoption and traditional support.

After all, we're talking about companies like Facebook (now Meta) pushing the metaverse so hard that even their company name changed to reflect it.

On the other hand, we have companies like Adidas, Shopify, Coca-Cola, and McDonald's venturing into this, publishing their own NFTs and creating interactive experiences in some metaverses. Samsung has its own "shop" in Decentraland.

And it gets more interesting; even within the metaverse sector, not all projects have experienced the same highs and lows.

The Sandbox (not the best performer in the sector) lost 20% less than other actors, such as Axie infinity (one of the most affected). In other words, the return is different for all participants, even within the same sector.

The more established sectors felt less of the impact.

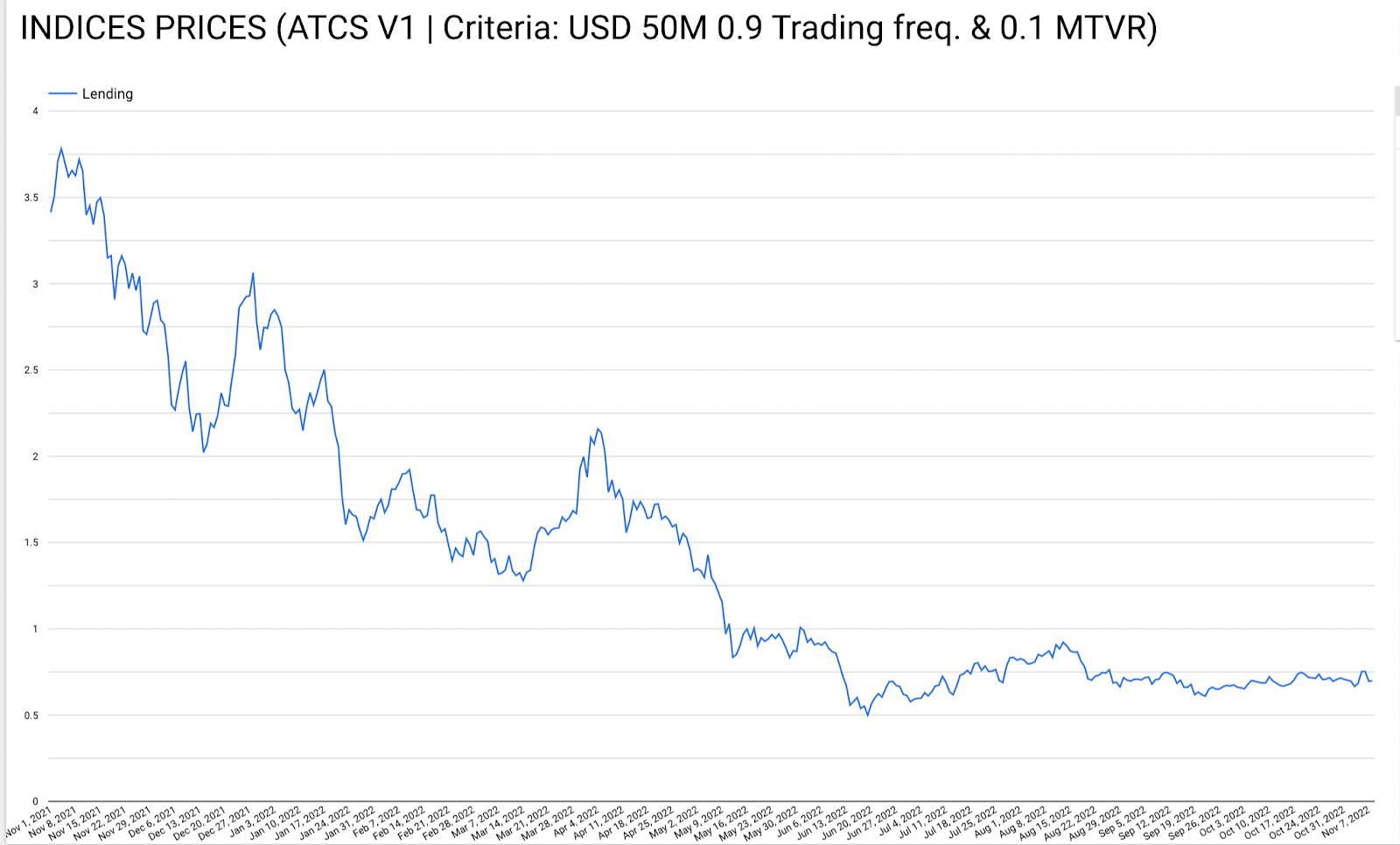

The Lending sector is one of the most established regarding Web3 use cases.

Its growth has been so significant that between 2020 and 20221, the TVL - or the amount of money that is "locked" in the protocol's smart contracts - went from $1 billion to $65 billion (today, the TVL is more than $18 billion). Only last year, $200 billion were given as loans from the most prominent lending protocols.

This sector lost 3.08 points or 81.5% from its highest prices, which is a smaller drop than the metaverse and shows that loans are achieving their product market fit.

But like when we talk about the metaverse, this sector's constituents behaved differently. Projects like Maple lost just 56% to their ATH, while Spell lost 97%. A forty-one percentage points difference between one and the other.

Blockchain project foundations continue to develop.

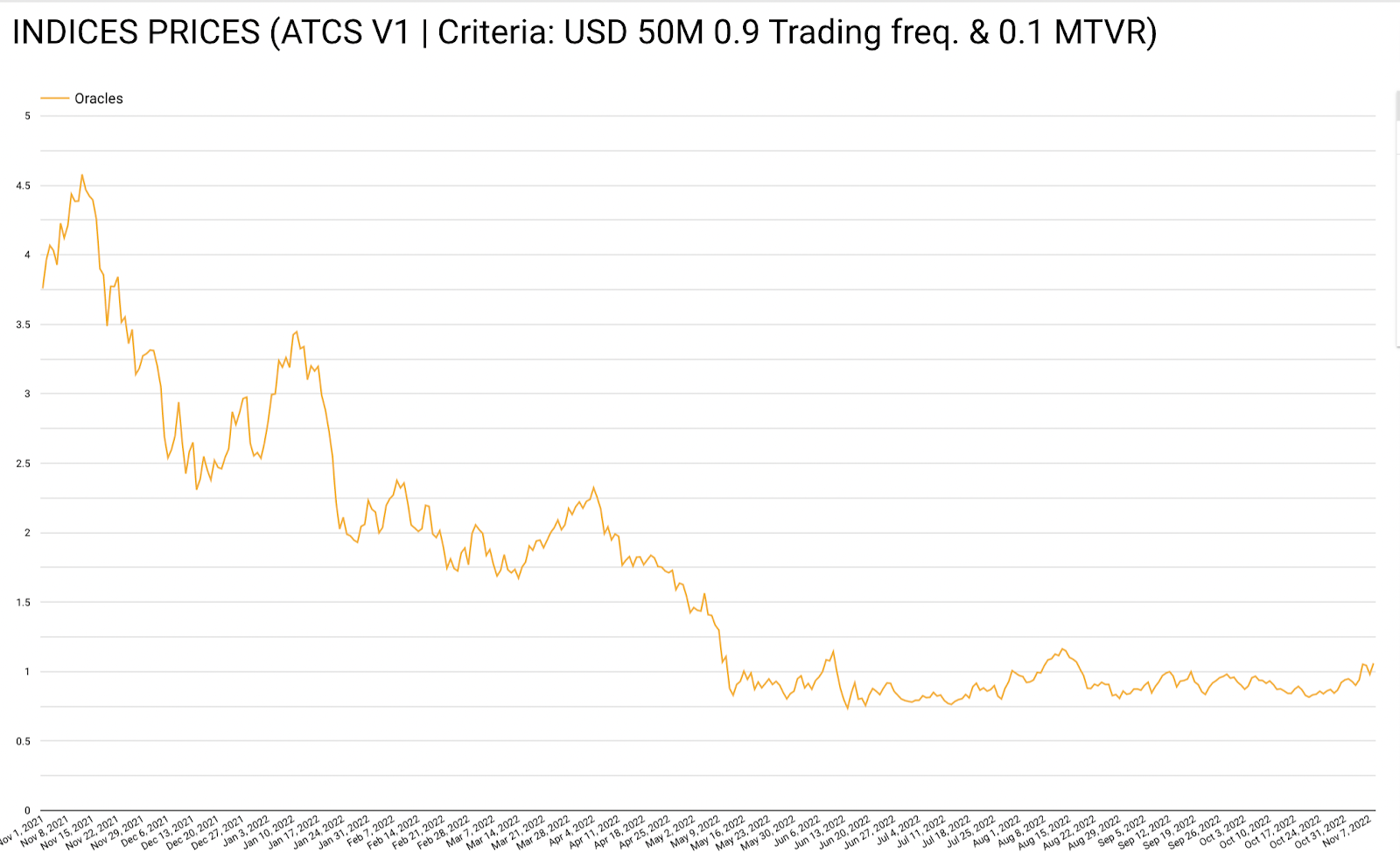

Oracles, explained simply, are protocols that allow data from the traditional and off-chain world to connect with on-chain data. They act as a bridge that connects the blockchain world with the conventional world.

Oracles are one of the foundations of crypto projects, and many of the Dapps, Play2Earn games, marketplaces, and exchanges depend on them to deliver reliable data. They are one of the pillars of networks.

The oracle sector lost 3.4 points or 76.9% from its peak prices. But here, the information gets more interesting.

Not all the projects that make it up lost; some, like Nest Protocol, increased their value by 21% compared to last year.

Nest is a protocol that seeks to quickly and accurately deliver prices to other DeFi protocols.

Let's remember that the lending and decentralized finance sectors as a whole were among the least affected by this crypto winter.

All projects exceed their 2020 prices.

One of the most common phrases, when we talk about crypto markets, is "when in doubt, zoom out," which applies in this case.

The metaverse sector - which, as we saw before, has lost more than 21 points from its highest point - is 7.98 points higher than 2020, or 1,123% growth in two years.

The lending sector - one of the least affected but which lost 3.08 points compared to its peak - is 0.56 points higher than in 2020, with 82.1% growth and 1,700% growth in its TVL.

Price, value, and the correct times to enter the market.

All investors are familiar with the famous phrase, "time in the market is better than timing the market."

But beyond the fact that there is no perfect time to enter markets and that the best strategy for passive investors is to enter and have a long-term view of their portfolios, it's essential to ask whether value and price are the same. And the answer is no.

Just under a year ago, many investors were willing to pay up to 97% more for some of the crypto projects than they are willing to pay today.

But the projects have a higher intrinsic value; we could argue that many have increased their value through significant developments and more active users.

Seeing also that the bases and infrastructure of the industry continue to develop - the infrastructure sector is practically at the same levels as 2020 and only 2.59 points lower than its ATH - we can argue that crypto projects can withstand the onslaught of inflation, highly volatile financial markets, recession, shocks of the Russo-Ukrainian war, and FED interest rate hikes.

This brings us to the importance of diversified portfolios.

As we have seen, only some sectors behaved similarly, and not all industry constituents had a similar performance.

This is why when it comes to investing, it is so essential to see crypto as something different than a unified asset class but to evaluate projects and sectors for what they are: unique market participants.

And that is why, as in the traditional financial market, it is so important to have a diversified portfolio of assets that gives broad exposure and reduces the impact of volatility.